Asset Pricing in a Concentrated Economy

Abstract

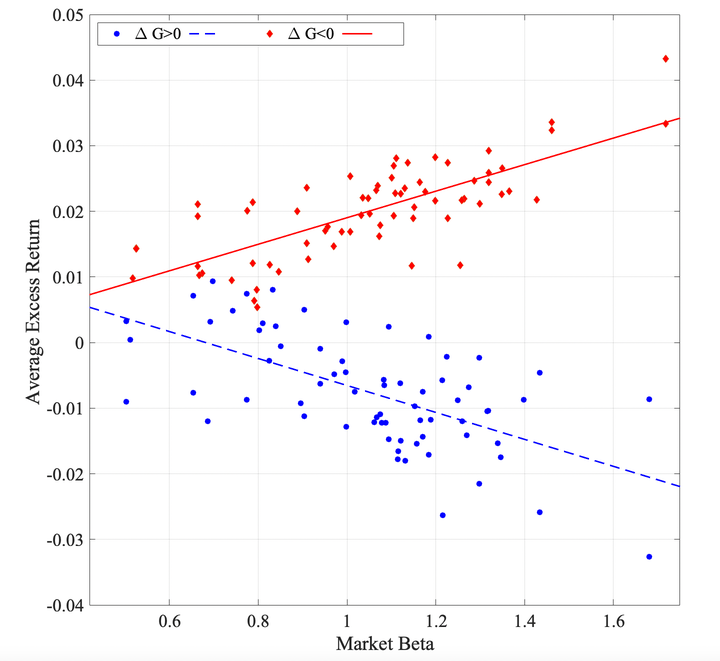

Market concentration drives the cross-sectional price of systematic risk. We develop a general equilibrium asset pricing model in which the distribution of firm sizes governs expected returns. Kimball demand gives larger firms higher markups, so rising concentration raises aggregate profits today; creative destruction then weakens as incumbents dominate, slowing productivity growth tomorrow. Higher concentration is therefore associated with lower expected dividend growth in the model, qualifying it as an observable long-run-risk state variable under recursive preferences. We take this mechanism to U.S. equity data from 1973 to 2024. Rising concentration coincides with macroeconomic and financial bad- state variables. Exposure to concentration risk is priced negatively in the cross-section, and the pricing is orthogonal to the Fama–French factors. The slope of the Security Market Line flips from positive in falling-concentration months to negative in rising-concentration months. The concentration premium is most visible in the Betting-Against-Beta strategy, which earns 3.7% per month more when concentration rises than when it falls. These results identify the industrial structure of the economy as an observable source of time-varying risk prices.

Best Paper Award in Asset Pricing — 2026 SAIF Annual Research Conference

Ali Shirazi

Assistant Professor of Finance

My research interests include Asset Pricing, Granular Economies, and Corporate Bond Markets.